What the researchers set out to measure

Evelyn Yee-Foon Kong and Kin-Boon Tang of Nottingham University Business School Malaysia examined 571 IPOs listed on Bursa Malaysia from January 2000 to December 2020. Their question was twofold: do Malaysian IPOs beat or trail the market once the listing-day excitement fades, and does investor sentiment at the time of listing help predict that outcome? Most local research stops at first-day returns. This one runs the clock out to 48 months and builds a dedicated sentiment index to test the behavioural side.

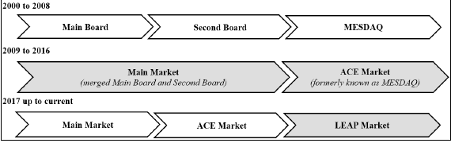

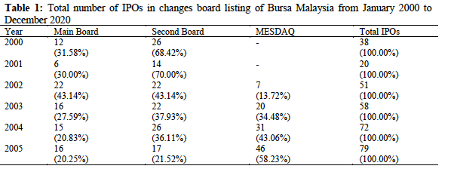

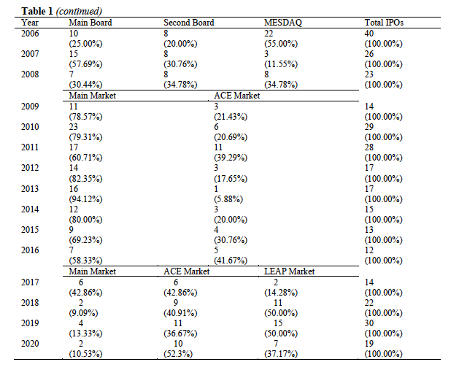

The sample period was chosen for a reason. It captures the merger of the Main and Second Boards into the Main Market, the rebranding of MESDAQ into the ACE Market in 2009, and the launch of the LEAP Market in 2017. Two decades of structural change, in other words, with a shifting mix of investors and listing standards underneath.

The headline: persistent underperformance

The study asks a simple question: if an investor bought a Malaysian IPO at the first closing price and held it for four years, did it beat the market?

The answer is: for many IPOs, no. When each IPO is treated equally, the average IPO performed about 19 percentage points worse than the FTSE Bursa Malaysia Emas benchmark after four years. The paper says this result is statistically strong, meaning the weakness was unlikely to be random.

The picture looks much better when bigger IPOs are given more weight. In that case, the underperformance was less than 2 percentage points after four years. This means large IPOs were close to the market’s performance. The bigger problem came from smaller IPOs, which pulled down the average.

The simple lesson: not all IPOs performed badly. Bigger IPOs were more stable, while smaller IPOs caused most of the long-term weakness.

A worked example

Picture two retail investors, each putting RM10,000 into the average Bursa IPO at its first closing price and holding for four years. The one who spread money across listings of every size — the equal-weight approach, which a small-cap-heavy IPO basket resembles — would end up around RM1,900 behind where the broad market would have left them. The one whose money sat mostly in the larger listings would trail by a few hundred ringgit. Same strategy, very different result, driven by the size of what they bought.

Where sentiment comes in

The researchers did not study company characteristics alone. They created a Malaysian IPO market sentiment index using trading activity, the number of IPOs, first-day returns, dividend behaviour, new equity issues, consumer confidence and business confidence.

They applied three statistical methods to construct the index. Each method found that sentiment was linked to long-term IPO performance, but the direction of the effect was not fully consistent. The sPCA and PLS models showed that stronger sentiment was associated with weaker long-term abnormal returns. This supports the idea that optimism can raise IPO prices too far, followed by a later correction.

The standard PCA model produced the opposite result: stronger sentiment was associated with better long-term returns. The safest conclusion is not that optimistic markets always lead to poor IPO performance. It is that market sentiment contains useful information, though the precise direction depends on how sentiment is measured.

Other factors that affected IPO performance

Market sentiment was not the only factor linked to long-term IPO performance. The study found several other patterns.

IPOs with very large first-day price gains often performed worse over the next four years. This suggests that investors may become too excited on listing day and push the price too high. Once the excitement fades, the share price may fall closer to its fair value.

Larger IPO offers were linked to weaker returns compared with the wider market. IPOs led by a major underwriter, such as CIMB, Maybank or RHB, tended to perform better. Companies listed on the Main Market also tended to achieve better results than those listed on the ACE Market.

The company’s age, number of board members, market volatility before listing and level of IPO oversubscription were linked to long-term performance too. This means investors should study more than the first-day price movement when judging an IPO.

One factor did not appear to matter: the percentage owned by major shareholders. Most Malaysian IPOs have a similar ownership structure. Bursa requires at least 25% of the shares to be held by the public, and founders or family members often retain much of the rest. Since ownership levels were similar across many IPOs, the researchers had little difference to compare.

Simple lesson: A very strong first-day gain does not mean the IPO will remain a strong investment. The underwriter, listing market, company background and market conditions may provide more useful clues about long-term performance.

The behavioural tension beneath the results

At first, the behavioural evidence appears to conflict with the study’s main finding. Earlier research cited by the authors suggests that some Malaysian investors sell underpriced IPOs too quickly. These investors receive shares at the offer price, enjoy an immediate gain on listing day, and sell early to protect that profit. In certain underpriced IPOs, the price continues rising after they exit, so they leave part of the gain behind.

The study’s four-year result examines a different situation. It measures performance from the first-day closing price, rather than from the original offer price. An investor entering at that point has already missed the listing-day gain and may be buying after optimism has pushed the share price higher. Across the full sample, IPOs bought at this closing price tended to trail the market during the following four years.

Contradiction? An IPO can be underpriced at the offer stage, rise sharply on listing day, continue performing well for a period, and still produce weak returns when measured from the elevated first-day closing price over four years. The studies cited on the disposition effect refer to selected underpriced IPOs and investor selling behaviour. The paper’s long-run result refers to the average performance of 571 IPOs relative to the market.

The paper adds another qualification: frequent traders tend to show a weaker disposition effect, and frequent trading is common in Malaysia. Trading experience may reduce the tendency to sell winners too early, though it does not eliminate the broader risk of buying IPOs after sentiment has driven up their prices.

For a Bursa trader, the lesson is not that selling on listing day is always wrong, nor that holding for four years is always worse. The entry price and the individual IPO matter. Subscribers buying at the offer price may capture a genuine listing gain. Investors buying at the first close face a different trade, and the study finds that this second group, on average, was poorly rewarded for a long holding period.

Honest limitations

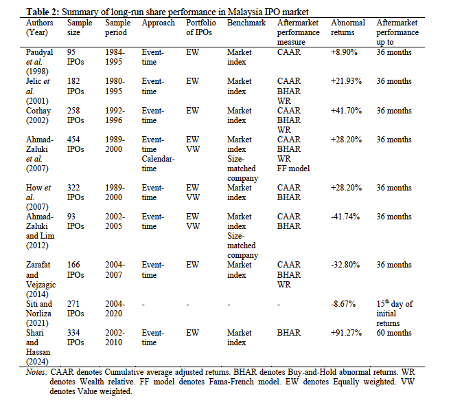

A few caveats keep this in proportion. The findings are specific to Malaysia, a developing market with low IPO volumes and a high delisting rate, and may not travel to other markets. Firms with incomplete data, those undergoing mergers, and delisted companies were excluded, thereby trimming the harshest failures from the sample. The study leans on a single benchmark, the FTSE Bursa Malaysia Emas Index, where some prior work uses several. And long-run IPO results are famously sensitive to method — the same data can show overperformance under one measure and underperformance under another, a point the authors acknowledge directly.

Reference

Kong, E. Y.-F., & Tang, K.-B. (2025). Unveiling the role of market sentiment in explaining Malaysian IPO aftermarket share performance. Capital Markets Review, 33(1), 41–73. https://www.mfa.com.my/cmr/v33_i1_a3/

This content is for educational purposes only and does not constitute financial or investment advice. Conduct your own research or consult a licensed financial adviser before making investment decisions.