Why “How”, Not “What”

Howard Marks, co-founder of Oaktree Capital, gives his talk a deliberate title: how to think about risk, not what to think about it. The distinction carries the whole argument. Marks is not handing investors a checklist of dangerous assets to avoid. He is trying to rewire the mental model itself — the way a retail investor on Bursa Malaysia, or a fund manager in KL, decides whether a return was earned skilfully or stumbled into by luck.

His opening claim sets the tone: risk is the real test of an investor’s skill, and the return on its own tells you almost nothing.“The return alone doesn’t tell you how good a job the manager did. The key question is — how much risk did the manager bear to get that return?”

The Return Is Only Half the Test

Marks walks through a set of managers in a market that rises 10% or falls 10%. The exercise exposes how empty a headline number can be.Manager Up market

| Manager | Up market (+10%) | Down market (−10%) | Verdict |

| A | +10 | −10 | Tracks the index — no skill |

| B | +20 | −20 | Pure aggression — no skill |

| C | +5 | −5 | Pure defence — no skill |

| D | +15 | −10 | Better upside, market-level downside — value added |

| E | +10 | −5 | Market upside, softer downside — value added |

Managers B and C produce different numbers from the index, yet neither shows judgement — one dialled up risk, the other dialled it down.

The investors worth paying for are D and E. They capture the gains when markets rise and lose less when markets fall.

Marks calls this property asymmetry, and he returns to it as the single trait that separates a skilled investor from a lucky one. Usually, a unit-trust factsheet quoting a three-year return tells you the size of the gain. It says nothing about which of these five managers produced it. These are usually easier to detect in a fixed-income fund. Where the paper usually has a rating.

Risk Is the Probability of Loss — Not Volatility

The academic finance taught at Chicago in the early 1960s, where Mark studied, adopted volatility as the measure of risk. His view: volatility was chosen mainly because it can be measured, and nothing better could be measured. He treats it as a symptom rather than the disease.

For Marks, risk is the probability of permanent loss. That maps onto what most people mean by the word. No one at Oaktree, he points out, refuses an investment for being volatile — they refuse it when the chance of losing money runs too high, or they demand a higher return to compensate for that chance.

You Cannot Measure Risk in Advance — or Even Afterwards

Here, Marks makes his most unsettling point. Risk cannot be quantified before the fact, and — the part most people miss — it cannot be quantified after the fact either.

Buy something for one ringgit, sell it a year later for two. Was it risky? The outcome cannot answer that. The investment might have been close to certain to double, or a reckless bet that happened to pay off. The result looks identical from the outside. A profitable trade may have carried enormous hidden risk that simply never surfaced. This is why Mark distrusts any system that converts risk into a precise number — the number describes the past distribution, not the probability that mattered.

The Many Faces of Risk

Loss of capital is only one form of risk. In his memos, Howard Marks identifies nearly two dozen others. Two are especially relevant for Malaysian retail investors.

The first is the risk of missing out—not in the sense of chasing trends, but in being overly conservative. Investors who allocate too heavily to fixed deposits or low-yield instruments may preserve capital, yet fail to grow it meaningfully over time.

The second is what Marks calls the cardinal sin of investing: selling at the bottom. Buying at a high price and enduring a decline is uncomfortable, but markets tend to recover over time, with future peaks often exceeding previous ones. Selling at the trough, however, converts a temporary paper loss into a permanent one and removes the investor from the eventual recovery.

Yes, a table helps. It separates the idea, meaning, and investing lesson.

More Things Can Happen Than Will Happen

Howard Marks borrows a line from a London Business School professor that captures one of his central ideas:

“More things can happen than will happen.”

The future is not one fixed outcome waiting to be predicted. It is a range of possible outcomes. Many things can happen, but only one thing will happen.

| Idea | What it means | Investing lesson |

| 1. Many outcomes are possible | For any future event, several things could happen. We cannot say with certainty which one will occur. | Do not build an investment case around only one expected outcome. |

| 2. The future is a probability distribution | The future should be viewed as a set of possible outcomes, each with a different likelihood. | Good investing is not about perfect forecasting. It is about judging odds, risk, and payoff. |

| 3. Probability is not certainty | Even when the odds are clear, the actual outcome can still surprise us. In backgammon, the dice probabilities are fixed, yet no one can say what the next roll will be. | A high-probability outcome can still fail. A low-probability outcome can still happen. |

| 4. Expected value can mislead | The average of possible outcomes may produce a number that will never actually occur. For example, the average of 2, 4, 6, and 8 is 5, but 5 is not one of the possible outcomes. | Investors should not rely only on the average expected return. They must also ask: “What can go wrong?” |

| 5. Ruin matters more than average return | An investment may have a high expected value but still carry a small chance of total loss. | A sensible investor may prefer a slightly lower return if it avoids the risk of being wiped out. |

Marks uses this idea to warn against false precision. Finance often looks more mathematical and predictable than it really is. The world appears orderly most of the time, but extreme events sit outside the normal range.

Peter Bernstein liked a similar observation from G.K. Chesterton: the world looks a little more regular than it truly is. Mark’s friend expressed the same idea in market terms: most financial history lies within two standard deviations, but the events that truly matter often occur outside that range.

The core lesson is simple: investors should respect uncertainty. The point is not to predict one future perfectly, but to prepare for several possible futures, especially the damaging ones that most people ignore.

Yes, this section can be made clearer by splitting it into two ideas:

1 Risk changes when people change their behaviour

2 Risk is often invisible until something bad tests it

Risk Is Counterintuitive — and Perverse

Howard Marks makes a simple but uncomfortable point: risk is not always where people think it is.

| Example | What happened | What it teaches about risk |

| Dutch town without traffic signs | A Dutch town removed traffic lights, road signs, and road markings. Accidents fell, since drivers became more careful when they could no longer rely on clear rules and signals. | Safety devices can make people less careful. When people sense danger, they often behave more cautiously. |

| Climbers with better equipment | Climbing gear improved over time, but the fatality rate did not fall much. Climbers used the better gear to attempt harder and more dangerous routes. | Better protection does not always reduce risk. People may use the extra safety margin to take bigger risks. |

examples explain this well.

The lesson is that risk does not sit only in the activity itself. It also depends on how people behave.

Markets work the same way. A market is not safe or dangerous by itself. It becomes safer when investors are cautious, disciplined, and price-sensitive. It becomes riskier when investors become confident, careless, and convinced that nothing bad can happen.

This is the perverse part of risk: the most dangerous belief is the belief that there is no risk.

| Market situation | What the crowd thinks | What may actually be happening |

| An asset falls in price | “This is dangerous.” | The lower price may have made it safer, since less optimism is built into the valuation. |

| An asset rises in price | “This is a great investment.” | The higher price may have made it riskier, since more good news is already priced in. |

Marks’s point is not that falling assets are always safe or rising assets are always dangerous. The point is that price changes risk. A good asset can become risky if the price is too high. A troubled asset can become safer if the price becomes low enough.

Risk Hides Until It Does Not

Marks then explains why risk is so hard to judge: risk is often invisible before loss appears.

Loss happens when hidden risk meets a negative event.

Warren Buffett’s image captures this perfectly: only when the tide goes out do you discover who has been swimming naked.

Marks gives another example. A house in California may have a construction flaw that causes no problem for years. The house looks safe. The flaw remains hidden. Then an earthquake comes, and the hidden weakness becomes an actual loss.

The same thing happens in investing.

| Before the event | After the event |

| The investment looks safe. | The hidden risk becomes visible. |

| No loss has happened for years. | One bad event causes major damage. |

| Investors become comfortable. | Investors realise the risk was there all along. |

This is why rare risks are so dangerous. An investment exposed to a rare disaster can look safe for a long time precisely because the disaster does not happen often. The long period without loss makes investors overconfident.

Marks connects this to the idea Nassim Taleb called the Black Swan: a rare, extreme event that many people ignore until it arrives. The overlap is close. Taleb explains the hidden tail risk as a philosopher of uncertainty. Marks describes it as a working-credit investor who has seen how hidden risks become real losses.

The core lesson is simple: risk is often highest when people believe it is lowest.

This is strong. I would make the logic cleaner by separating asset quality from price paid.

It Is Not What You Buy, It Is What You Pay

Howard Marks rejects a common investing mistake: the idea that high-quality assets are always safe and low-quality assets are always risky.

His point is sharper than that. Safety does not come from quality alone. Safety comes from the relationship between quality, price, and risk.

His point is sharper than that. Safety does not come from quality alone. Safety comes from the relationship between quality, price, and risk.

| Common belief | Marks’s correction |

| Good companies are safe investments. | Good companies can be dangerous if bought at too high a price. |

| Weak companies are bad investments. | Weak companies can be good investments if the price is low enough. |

| Risk comes mainly from the asset. | Risk often comes from overpaying. |

| Quality protects investors. | Price is what protects investors. |

Marks learned this through two opposite experiences.

| Example | What happened | Lesson |

| The Nifty Fifty | In the late 1960s and early 1970s, investors loved the top growth companies in America. These were seen as such strong businesses that no price seemed too high. Many later produced terrible returns for investors who bought at the peak. | A great company can become a poor investment when the entry price is too expensive. |

| High-yield bonds | In 1978, Marks began investing in bonds issued by lower-quality companies. These companies were riskier, but the bonds were priced cheaply enough to compensate for that risk. | A lower-quality asset can be a good investment when the price already reflects the danger. |

This led Marks to one of his clearest conclusions:

Investment success does not come from buying good things. It comes from buying things well.

No asset is so good that it cannot become dangerous at the wrong price. Few assets are so poor that they cannot become attractive at the right price.

The Malaysian example is the glove sector in 2020. The glove companies were real businesses with real earnings during the pandemic boom. Demand was strong. Profits were high. The problem was not that the businesses were fake.

The problem was the price investors paid.

At the peak, the market treated glove stocks as if extraordinary profits would continue for a long time. When demand normalised and earnings fell, the share prices collapsed. The loss came less from the product and more from the valuation.

That is the Bursa Malaysia version of the Nifty Fifty lesson: a good story can still become a bad investment when the price is too high.

This idea is good, but the key sentence should be simpler: higher risk does not guarantee higher return; it only requires the possibility of higher return.

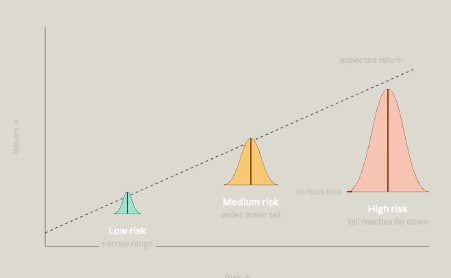

The Risk–Return Line Everyone Misreads

The textbook chart shows a straight upward line: as risk rises, expected return rises too.

Many investors read this wrongly. They think it means:

| Common reading | Why Marks says this is wrong |

| Riskier assets deliver higher returns. | If higher returns were guaranteed, the assets would not be risky. |

| To make more money, take more risk. | More risk means a wider range of outcomes, not a certain higher return. |

| Risk is rewarded automatically. | Risk is only rewarded when the price is right and the outcome works out. |

Marks’s correction is simple: riskier assets must offer higher expected returns to attract buyers, but they do not have to deliver those returns.

The word expected matters.

An asset may be priced to offer a high return, but the actual result can still be poor. The risk sits in the gap between what investors expect and what actually happens.

Marks redraws the textbook chart in a better way. Instead of one clean upward line, each level of risk should have a range of possible outcomes

| Move along the risk line | What happens |

| Expected return rises. | Investors demand more return for accepting more uncertainty. |

| The range of outcomes widens. | Results become less predictable. |

| The bad outcomes get worse. | The downside becomes more severe. |

| The left tail stretches further. | The chance of serious loss becomes more meaningful. |

That wider range is the real meaning of risk.

A low-risk asset may have a narrow range of outcomes: the return is unlikely to be very high, but the loss is also limited. A high-risk asset may have a higher expected return, but the possible outcomes are much wider. It may do very well, perform poorly, or cause a large loss.

The core lesson is this: risk does not promise return. Risk creates uncertainty. The investor is paid only if the price is cheap enough and the future turns out well enough.

This is already clear, but it can be made more readable by spelling out the bowl idea step by step.

One Ticket From the Bowl

Marks describes investment results as one ticket drawn from a bowl.

Inside the bowl are many possible outcomes. Some tickets are good. Some are bad. Some are excellent. Some are painful. When we invest, only one ticket is drawn.

The investor does not control which ticket comes out.

The better investor has a different advantage: they understand the mix of tickets in the bowl better than others.

| What the bowl represents | Meaning in investing |

| Many tickets in the bowl | Many future outcomes are possible. |

| One ticket is drawn | Only one actual result will happen. |

| Winning tickets | The investment produces a good return. |

| Losing tickets | The investment loses money or disappoints. |

| The mix of tickets | The probability distribution of possible outcomes. |

| How much you stake | Position sizing and risk control. |

The superior investor is not superior because they can predict the exact ticket that will be drawn. They are superior because they judge the bowl more accurately.

They ask better questions:

| Question | Why it matters |

| Are there more winning tickets than losing tickets? | This tells us whether the opportunity is attractive. |

| How large are the winning tickets? | This shows the upside. |

| How painful are the losing tickets? | This shows the downside. |

| Can I survive the worst tickets? | This decides how much money to put in. |

This changes the whole meaning of investment skill.

Skill is not about saying, “This will happen.”

Skill is about saying, “These are the possible outcomes, these are the rough odds, this is the likely reward, this is the possible damage, and this is how much I should risk.”

The key lesson is simple: good investors do not try to control which ticket comes out. They study the bowl, then size the bet so that one bad ticket cannot destroy them.

This section is good, but the main point can be clearer: risk control is not something you switch on only when trouble appears. It must be present before trouble arrives.

Handling Risk: Continuous, Not “Risk-On, Risk-Off”

Marks dislikes the common market language of “risk-on” and “risk-off.”

That language makes risk management sound like a switch: investors take risk when markets are calm, then turn defensive when danger appears. Marks thinks this is misleading. Bad events do not announce themselves in advance. No one rings a bell before a crisis, a credit problem, or a market collapse.

Risk control must be built into the portfolio before a bad event occurs.

Marks uses football to explain this. In American football, teams have separate attacking and defensive units. The game stops often, and players can be replaced depending on the situation.

Soccer is different. The same eleven players stay on the pitch. They must attack and defend as the match develops. There are fewer pauses. No referee stops the game to tell the team when to change from offence to defence.

Investing is closer to soccer.

| Bad reading of risk | Marks’s reading of risk |

| Risk control can be turned on later. | Risk control must be present from the start. |

| Investors can wait for clear warning signs. | Warning signs are often clear only after damage is done. |

| Offence and defence are separate phases. | Offence and defence must work together continuously. |

| The market gives time to adjust. | The market often moves before investors are ready. |

The investor’s task is not to be aggressive one day and defensive the next based on market mood. The real task is to decide, continuously, how much offence and how much defence the portfolio should carry.

Marks’s insurance examples make the idea more practical.

We buy motor insurance every year. In years with no accident, we do not say the insurance was useless. The protection had value because it covered a risk that could have appeared.

Life insurers operate in a similar way. They take risk, but they do not take it blindly. They study the risk, spread it across many people, and charge a premium for carrying it.

Marks says Oaktree approaches credit in the same spirit.

| Insurance company | Oaktree’s credit investing |

| Studies the risk before accepting it. | Studies the borrower, asset, structure, and downside. |

| Diversifies across many policies. | Diversifies across many credit positions. |

| Charges a premium for bearing risk. | Demands extra yield for accepting credit risk. |

| Accepts that some claims will happen. | Accepts that some defaults or losses may happen. |

The point is not to avoid risk completely. The point is to take risk intelligently.

Good risk-taking has four parts: understand the risk, price it properly, diversify it, and make sure the potential reward is enough.

The core lesson is simple: risk management is not a market-timing switch. It is a continuous discipline.

This is a strong closing section. I would make it cleaner by separating Marks’s conclusion from your caveats.

Asymmetry: The Cornerstone

Marks’s whole argument returns to one idea: asymmetry.

The skilled investor does not try to remove risk completely. Instead, they try to build a portfolio that can do two things at once:

| If things go right | If things go wrong |

| The portfolio earns a good return. | The portfolio does not suffer permanent damage. |

That is the real goal of superior investing: capture enough upside, but limit the downside.

This is hard to see in normal times. Risk control often looks unnecessary when nothing bad happens. A cautious investor may appear too conservative during a rising market. The value of that caution only becomes clear when markets are tested.

This is why Marks keeps returning to the image of the tide going out. You only discover who was exposed after conditions change.

The prudent investor accepts this quiet trade-off. They take comfort in knowing that risk is under control, even during long periods when that risk never appears.

Marks is not saying investors should avoid risk completely. That would mean avoiding a return too. His message is more balanced

| Wrong approach | Better approach |

| Avoid all risk. | Manage risk intelligently. |

| Chase return without protection. | Seek return with the downside controlled. |

| Assume good times will continue. | Prepare for outcomes that may hurt. |

| Focus only on expected return. | Study both upside and downside. |

The aim is not risk avoidance. The aim is good risk-bearing: accept risk only when it is understood, priced properly, diversified, and compensated.

Caveats: Where Marks Is Helpful, and Where He Is Incomplete

Marks gives investors a powerful way of thinking, but it should not be treated as a full manual.

| Caveat | Why it matters |

| He gives a mindset, not a formula. | “Read the distribution of tickets in the bowl” is a sound idea, but difficult to apply. Retail investors often lack the data, time, and experience to judge the full range of outcomes. |

| Risk cannot be fully quantified. | This is useful because it protects investors from false precision. Yet it is also inconvenient, since beginners must rely on judgement they may not have developed yet. |

| The examples are mostly from US institutional markets. | The Nifty Fifty and high-yield bond examples are powerful, but they come from a deep US market. The principle travels, but the instruments do not map perfectly onto Bursa Malaysia. |

| The talk is a summary, not the full system. | Marks is compressing ideas from his memos and books. The talk gives the skeleton, not the full body of evidence and application. |

The fairest reading is this: Marks is not giving investors a checklist to follow mechanically. He is teaching the judgment behind good investing.

The core lesson is simple: superior investing is not about avoiding risk. It is about taking the right risks, at the right price, in the right size, with the downside kept under control.

Yes. To make it more critical thinking, the final assessment should not sound like pure praise. It should show what Marks gets right, where the idea is useful, and where it has limits.

Final Assessment

Marks’s main value is that he changes how investors judge success. A good return alone does not prove skill. The real question is how much risk was taken to earn that return.

For Malaysian retail investors, this lesson is useful. Bursa often rewards chasing hot stocks, treating quick gains as proof of ability, and selling in panic when prices fall. Marks pushes investors to think differently: focus less on prediction and more on preparation.

The strongest idea is asymmetry. Good investing is not about avoiding risk completely. It is about taking risk only when the price, odds, and downside make sense. The aim is to earn enough when things go right, yet avoid serious damage when things go wrong.

The limitation is that Marks gives a mindset, not a formula. His examples come mainly from US institutional investing, especially credit markets. Bursa Malaysia is thinner and more sentiment-driven, so the same ideas need local adjustment.

The final lesson is simple: take risk only when you are paid for it, and never confuse a calm market with a safe investmen

Source: Marks, H. How to Think About Risk . The companion text is Marks, H. (2011). The Most Important Thing: Uncommon Sense for the Thoughtful Investor. Columbia University Press, and Oaktree Capital memos.

This content is for educational purposes only and does not constitute financial or investment advice. Always conduct your own research or consult a licensed financial adviser before making investment decisions.